The Discounted Cash Flow (DCF) method is a valuation technique used by investors (especially in later-stage funding rounds) to estimate a startup’s fair market value (FMV). It calculates the present value of the company’s expected future cash flows, discounted at a specific rate (WACC) that reflects the risk.

For early-stage Indian startups, the DCF method is primarily used as a sanity check or for regulatory compliance, as the high uncertainty in forecasting cash flows often requires blending it with market-based approaches like the VC Method or the Comparable Transaction Method.

The Founder’s Dilemma: Why DCF is Hard for Startups

The fundamental principle of valuation is straightforward: A company is worth the sum of all the cash it will generate in the future. This is what the DCF method measures.

However, applying this to an early-stage Indian tech startup presents three massive challenges:

- Forecasting Blackout: A newly incorporated startup often has zero revenue. Forecasting cash flows for the next 5-10 years becomes an exercise in educated guesswork, making the output highly sensitive to even minor changes in growth assumptions.

- Regulatory Burden: The Income Tax Act, 1961, and FEMA regulations mandate that shares issued to investors must be priced based on Fair Market Value (FMV), often determined by a merchant banker who uses DCF as a core component. Incorrect DCF compliance can lead to issues like the dreaded Angel Tax (Section 56(2)(viib)).

- High-Risk Discount Rate: Early-stage Indian ventures carry immense risk. The discount rate (or WACC) applied to the cash flows is extremely high, meaning the future value is drastically reduced in present-day terms.

Breaking Down the DCF Method: The Three Core Components

To perform a DCF valuation, you need three key inputs. Understanding how they are calculated in the Indian context is crucial.

1. Free Cash Flow (FCF) Projections

FCF is the cash generated by the company after accounting for cash outflows that support operations and capital expenditure (Capex).

- Startup Reality: For a young Indian startup, projections (typically 5 years) must be meticulously justified based on market size (TAM/SAM/SOM), customer acquisition cost (CAC), and expected churn rates in the Indian market. Auditors and investors will heavily scrutinize these assumptions.

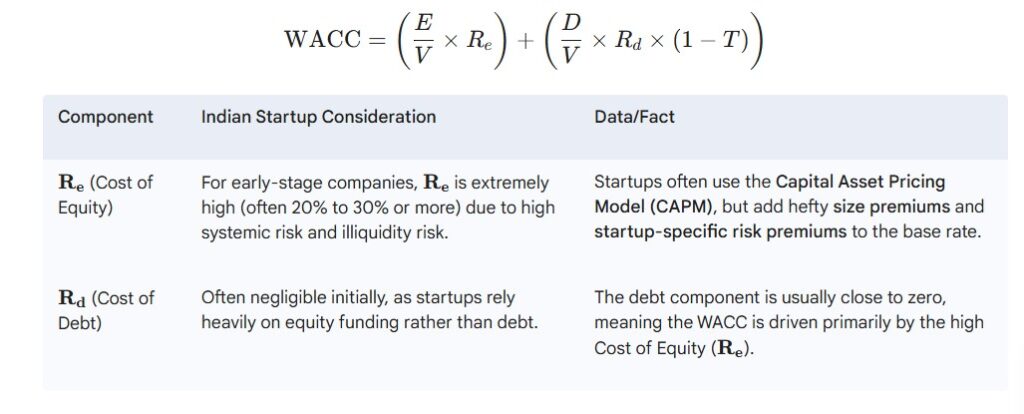

2. The Discount Rate: WACC in India

The discount rate, usually calculated as the Weighted Average Cost of Capital (WACC), represents the rate of return required by investors. This rate accounts for the risk associated with investing in the startup.

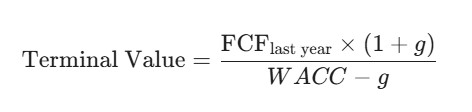

3. Terminal Value (TV)

The Terminal Value represents the cash flow generated by the company after the initial projection period (usually from Year 6 to infinity). For successful startups, this often accounts for 60% to 80% of the total DCF valuation.

Startup Reality: The stable growth rate (g) should reflect the industry’s long-term growth potential in India, usually around the long-term inflation or GDP growth rate (e.g.,3%-5%). An unusually high growth rate here is a major red flag to investors and regulators.

Illustrative Example: Simplified DCF for an Indian EdTech Startup

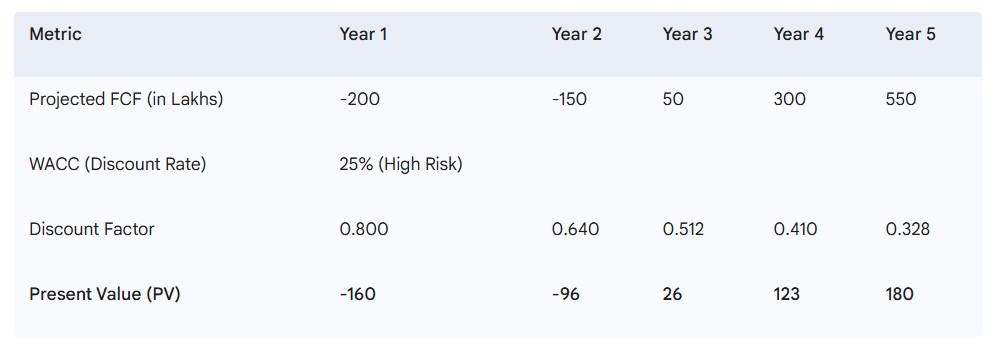

Let’s assume a hypothetical early-stage EdTech startup, EdConnect Pvt. Ltd., requires valuation for its Seed Round.

The total present value (PV) of cash flows from Year 1 to Year 5 is calculated as:

–160 – 96 + 26 + 123 + 180 = 73 lakhs

Next, the terminal value (TV) is computed using a perpetual growth rate of 4%:

TV = (550 × 1.04) / (0.25 – 0.04)

This gives:

TV = 572 / 0.21 ≈ 2,723 lakhs

To find the present value of this terminal value, it is multiplied by the Year-5 discount factor (0.328):

PV of Terminal Value = 2,723 × 0.328 ≈ 893 lakhs

Finally, the Enterprise Value (EV) under the DCF method is the sum of the present value of cash flows (73 lakhs) and the PV of the terminal value (893 lakhs):

EV = 73 + 893 = 966 lakhs,

which is approximately ₹9.66 crore.

The Coinshell Strategy: Blending Methods for Investor Readiness

While the DCF method provides an “intrinsic” value, it is rarely used in isolation for early-stage Indian startups. Coinshell advises founders to blend the DCF result with other, more market-friendly approaches to ensure investor confidence and compliance:

- Comparable Transaction Method (CTM): Benchmarking against recent funding rounds in similar Indian EdTech startups.

- Venture Capital (VC) Method: Back-calculating the required present valuation based on the expected future value upon exit.

- Scorecard Method: Adjusting the valuation of comparable companies based on qualitative factors (team quality, market opportunity, technology).

For regulatory valuation (like the FMV certificate needed for ROC/Income Tax compliance), the DCF acts as the critical anchor, providing the necessary legal justification required by Indian authorities.

FAQ

Q: What is WACC and why is it high for an Indian startup? A: WACC (Weighted Average Cost of Capital) is the discount rate representing the required return for investors. It is high for Indian startups because of the extreme risk of failure and lack of liquidity, often resulting in rates above 20%.

Q: Is the DCF method mandatory for startup valuation in India? A: DCF is one of the methods permitted by regulatory bodies (like the MCA/Income Tax Department) for determining the Fair Market Value (FMV) when issuing shares to non-residents or when dealing with certain tax exemptions.

Q: What is the biggest mistake founders make when preparing DCF projections? A: The most common mistake is using excessively optimistic, unsupported growth rates (especially the Terminal Growth Rate), which makes the valuation look unrealistic and undermines investor trust.

Ready to Nail Your Valuation and Compliance?

A robust, well-justified DCF is the hallmark of an organized, investor-ready startup. Don’t let compliance ambiguities delay your funding round or expose you to Angel Tax risk.

Coinshell specializes in creating Due Diligence-ready valuation reports and providing the required FMV certifications from our expert CAs and CSs.

Chat with our Experts today on whatsapp

- How to Build a Data Room in a Startup for Due Diligence ?

- Understanding the DCF Method for Early-Stage Startup Valuation in India

- ROC Scrutiny: Why It’s Increasing and How to Avoid Penalties

- Inter-Corporate Loans and Investments: What Startups Need to Know About Section 186

- Can a Private Limited Company Issue Public Debentures? A Legal Perspective